Blog

Why merchants should support pay by bank — before customers demand it

March 7, 2023

Editorial Team

According to the savings calculator on the Link Money homepage, the case for pay by bank is very clear. In fact, a (subscription) merchant with 100,000 customers and an average monthly transaction value of $12 will save more than half a million dollars in transaction fees annually if they utilize Link Money - Pay by Bank.

This is a compelling business case. However, some merchants may be wary of integrating a payment method that is relatively untested in the US market and may want to see how adoption looks before jumping in. And adding a new payment method is an important consideration — with all the priorities your business faces, you probably don’t want to spend time on integration unless you feel confident it has a high chance of success.

On that note, here are some reasons why clearing the adoption hurdle and seeing benefits may be easier and faster than you think.

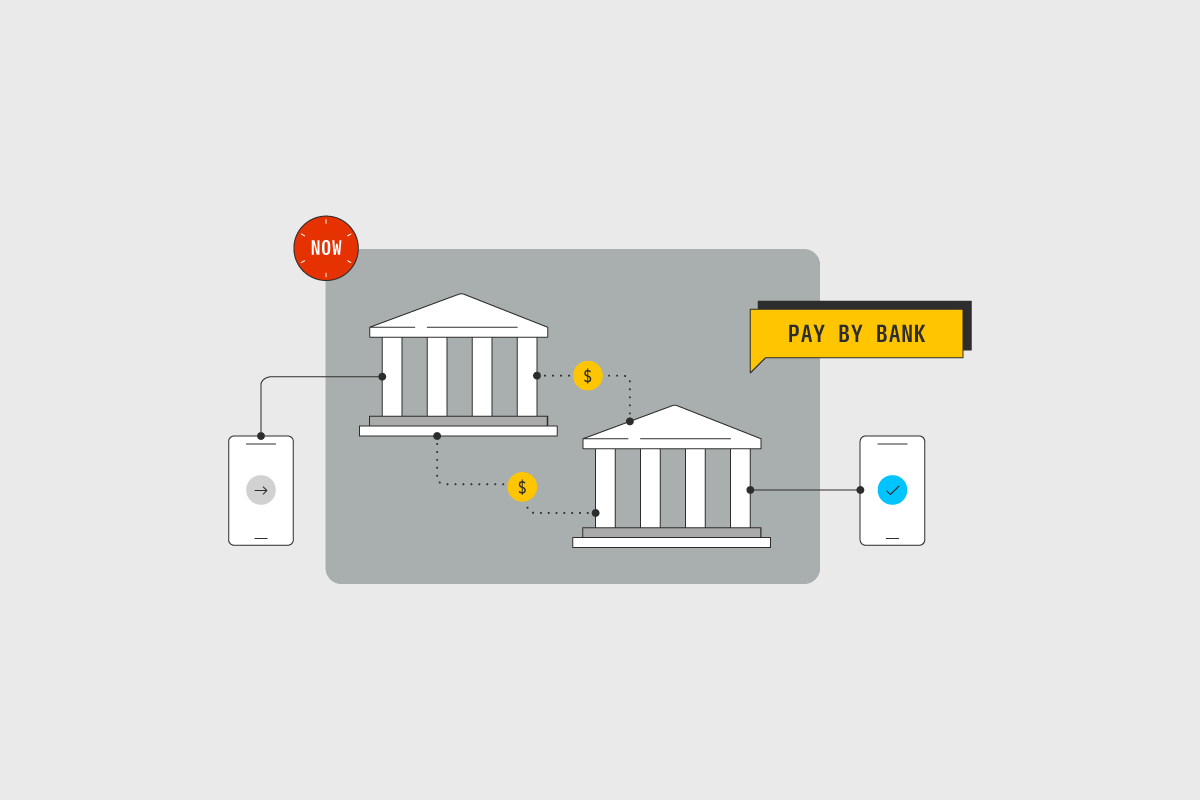

1. Pay by bank improves the customer experience

Pay by bank is an account-to-account (A2A) payment method, meaning that money is moved from the customer’s account to the merchant’s directly, with no debit or credit card required. Further, unlike many other payment methods, pay by bank does not require any new account creation or setup. This makes the payment experience extremely simple and easy, as can be seen in the flow below.

And beyond the payment experience itself, pay by bank:

Can be cheaper for the consumer, if the merchant decides to pass on savings on swipe fees.

Reduces the risk of fraud, since a bank account requires stronger authentication than cards.

Is very attractive to those who are averse to credit cards, since it is linked to their checking account rather than demanding they use credit. Likewise, it can be a compelling option for people who carry credit card debt but don’t want to add to it.

Is very attractive to subscription and recurring customers, since bank accounts do not get lost, stolen, or expire, meaning they will always have access to the service they are paying for.

All these factors combined lead to compelling advantages for your customers in terms of the payment experience.

2. The adoption curve of new payment methods can be blazing fast

On a related note, it is important to note that while cards — either directly or through wallets — underpin the majority of e-commerce transactions in the US, and have done since the advent of e-commerce, our payment culture is actually very dynamic.

A case in point: BNPL. This has quickly become a popular alternative to credit cards over the past few years as they removed complexity and fees for consumers. The growth is eye-popping — reaching an estimated 3.8% of the value of North American e-commerce sales in 2021, compared with 1.6% just one year earlier. Through its compelling advantages to consumers, BNPL is a good case study of just how fast newcomers can eat into incumbents’ market share, and how much pent-up demand for better choices beyond credit cards there really is.

The advantages to consumers of pay by bank are similarly compelling. With the right mix of merchant uptake and a little consumer education, pay by bank could be embraced by consumers just as quickly.

3. Your swipe fees will be reduced drastically and instantly

Money saved adds up quickly. Link Money - Pay by Bank costs merchants an estimated 70% less per transaction compared to credit cards. This is obviously a significant amount. But further to this, delaying a rollout of pay by bank also represents an opportunity cost.

To get a sense of how much you may be able to save on swipe fees, you need to establish a baseline with the payment method setup you are offering today.

How much do card swipe fees cost your business?

How much does payment fraud cost your business?

How much do other payment methods — wallets, BNPL, and so on — cost in fees?

If you are a subscription company, what is your rate of involuntary churn due to expired, lost, and stolen cards?

Pull these figures together and to help answer a key question: How much do payments (including involuntary churn) cost in fees, per day, month, and year?

With these figures, you will be able to run a projection on how much money you are spending unnecessarily on a daily basis by NOT offering pay by bank.

4. Your checkout conversion will improve immediately

While some cart abandonments are unavoidable, since website visitors may only be browsing, comparing prices, saving items for later, and so on, a huge percentage can be saved by optimizing the checkout and payment experience. In fact, in 2022 research across 4,000+ US adults, found that these percentages of shoppers abandoned their purchase at the checkout due to the following reasons:

18% didn’t trust the site with their credit card information

17% found the checkout process too long / complicated

4% experienced a declined credit card.

Offering pay by bank can reduce all of these risks. With the payment, no bank data is shared with the e-commerce site — the customer is redirected to their own bank environment where they authenticate the payment, reducing their concern about sharing credit card information on the merchant’s site. This also reduces the complexity of the checkout process, particularly if the customer’s payment can be quickly and seamlessly authenticated with biometrics or PIN. And because it is a direct transaction that moves money from one account to the other, as long as there are sufficient funds in the customer’s account, there is no reason for it to be declined.

Combined with lower swipe fees, increased conversion at the checkout can deliver sustainable and significant boosts to revenue.

And if you’re a subscription or recurring merchant, you have the most to gain

For subscription merchants, up to 48% of customer churn comes from failed payments, due to the inherent risks cards carry when it comes to subscription and recurring payments. If you are not focused on solving this issue, you are missing half of the challenge.

This is where pay by bank can play to its core strengths. The fact that no card is involved in the transaction completely removes the risk of expiration and loss since bank accounts do not expire, and cannot be lost. There is still a risk of insufficient funds, but providers such as Link Money are able to reduce this risk through predictive analytics and smart retries, drastically decreasing the rates of involuntary churn for subscription merchants.

Benefit from lower costs and improved conversion now

Pay by bank lowers the cost of doing business and improves the customer experience. It requires a minimal amount of education for customers, and the impact can be directly measured in dollars from day one of implementation. Furthermore, the technology is ready to go — providers such as Link Money have connections with well over 90% of US checking accounts, a figure that is only increasing.

Innovators that adopt this payment method will be able to reap the benefits of delivering a better customer experience, and spending less money on swipe fees, faster than their competitors. At a time when competition is heating up and economic uncertainty and inflation are still risks, this can mean outsized gains to the early movers.

To find out more about how your business can benefit from pay by bank, get in touch.